The Great Integration: How Washington Is Absorbing Crypto

The New Era of US Crypto Regulation

In 2025, U.S. crypto policy flipped. For years, the industry lived under “regulation by enforcement”—lawsuits instead of rules, old precedents stretched over new technology, markets whipsawed by headlines. Compliance was a guessing game, and talent fled to Europe and Asia where at least the rules were written down.

That changed this year. SAB 121, which had kept banks out of custody, was scrapped in January. Congress passed the GENIUS Act in June, giving stablecoins federal recognition and tying them to the dollar. And on September 2, the SEC and CFTC ended years of gridlock with a joint statement inviting exchanges like Nasdaq and CME to list spot Bitcoin and Ether under the same standards as stocks and futures.

Now there’s a path—narrow, but real—for projects to launch, banks to custody, and institutions to buy without fearing the rules will change in court. The message is clear: America wants crypto inside its financial system, and it intends to set the global standard for how that system runs.

The Era of Regulation by Enforcement (2021–Jan 2025)

For most of the past decade, crypto in the U.S. lived under a legal cloud. The SEC, led by Chair Gary Gensler, leaned on a seventy-nine-year-old precedent to define the entire industry: the Howey test.12 This Supreme Court case from 1946 decided that selling orange groves in Florida counted as an “investment contract” if buyers expected profits from the work of others. The logic—reasonable in the mid-20th century—was stretched to fit tokens, blockchains, and decentralized networks. If people bought a token with the hope that developers would make it more valuable, the SEC said it was a security. By that standard, almost everything in crypto could qualify.

Critics argued this wasn’t regulation at all, but a political and legal strategy to rein in the sector without giving it a path to comply. The results were years of courtroom battles instead of clear rules.

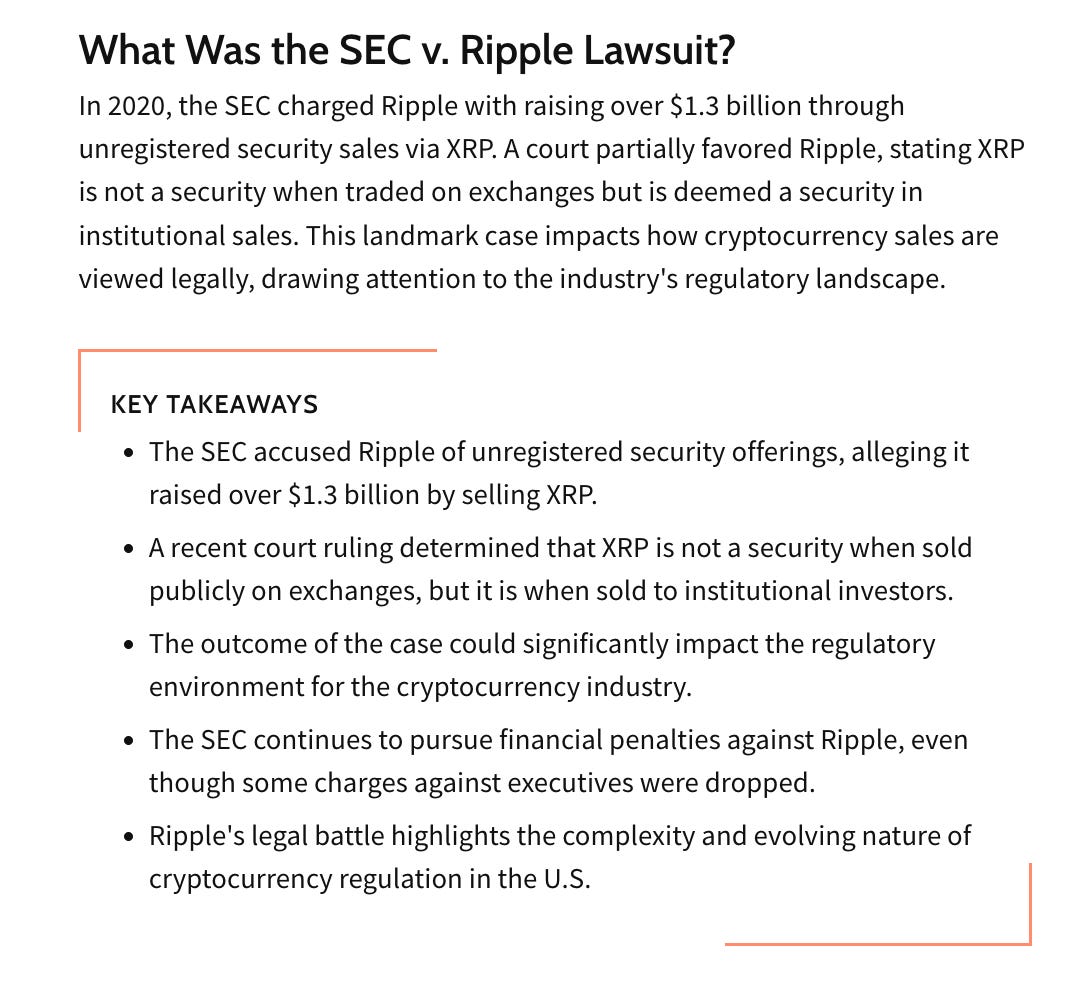

Ripple: one token, two legal identities.

The SEC’s lawsuit against Ripple Labs, filed in December 2020, accused the company of raising $1.3 billion through unregistered securities sales of its XRP token.

After years of litigation, Judge Analisa Torres delivered a split verdict in July 2023. She ruled that XRP wasn’t a security when sold on exchanges to the public—because retail buyers had no reason to expect Ripple’s work to drive their profits.

But XRP was a security when sold directly to institutions, where contracts and marketing tied the token’s value to Ripple’s efforts. The ruling created a strange precedent: one asset could be a security in one context and not in another. Exchanges and issuers were left with no certainty about what would trigger the SEC’s wrath.

Coinbase: approved, then sued.

The SEC’s case against Coinbase made the contradictions even sharper. Coinbase had gone public in 2021 with its S-1 registration statement formally approved by the Commission. Two years later, in June 2023, the SEC sued Coinbase for operating as an unregistered exchange, broker, and clearinghouse.

Coinbase fought back, pointing out that the agency had reviewed and signed off on its disclosures at IPO.

The company even tried an “equitable estoppel” defense, arguing that the government’s silence during its listing amounted to implicit approval, and that suing afterward was “affirmative misconduct.” The claim was legally ambitious, but it captured the frustration of an industry that felt set up to fail: no matter how it engaged with regulators, the rules would shift after the fact.

The cost of uncertainty.

Markets didn’t wait for final rulings. Academic event studies show that when the SEC labeled an asset a security, its price collapsed—down 5.2% within three days, and more than 17% within a month.

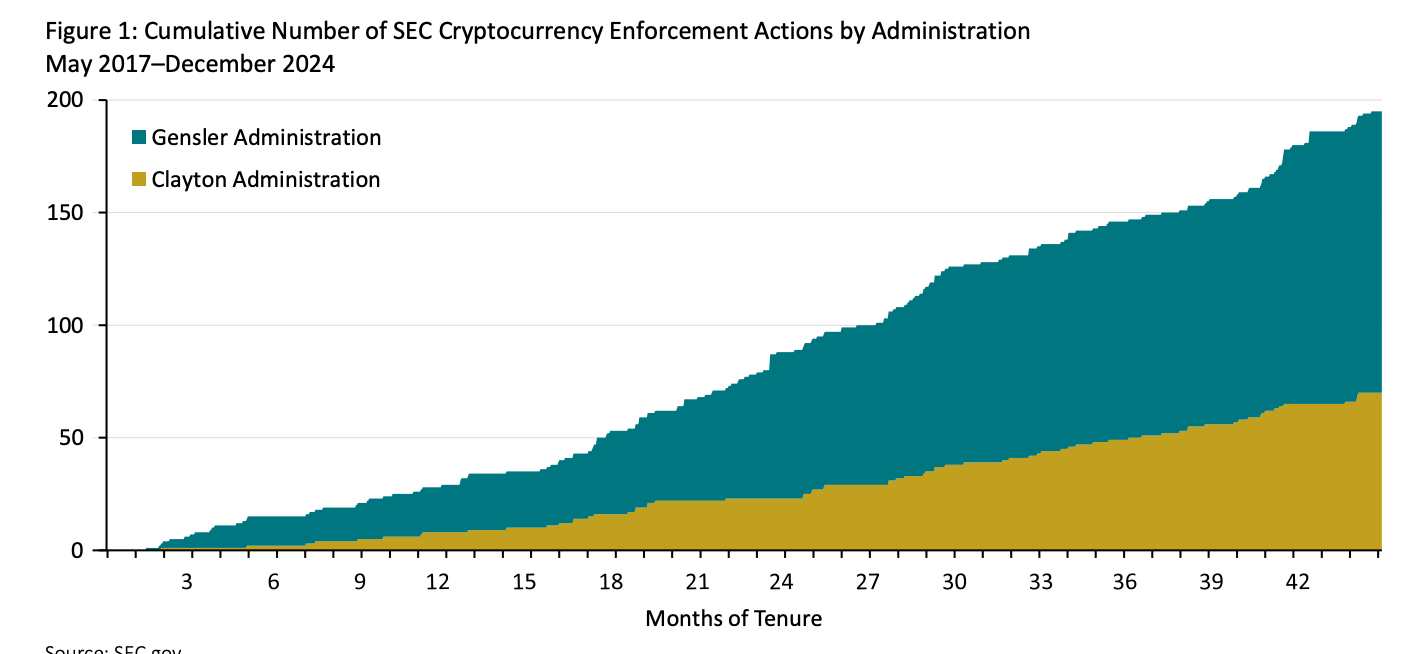

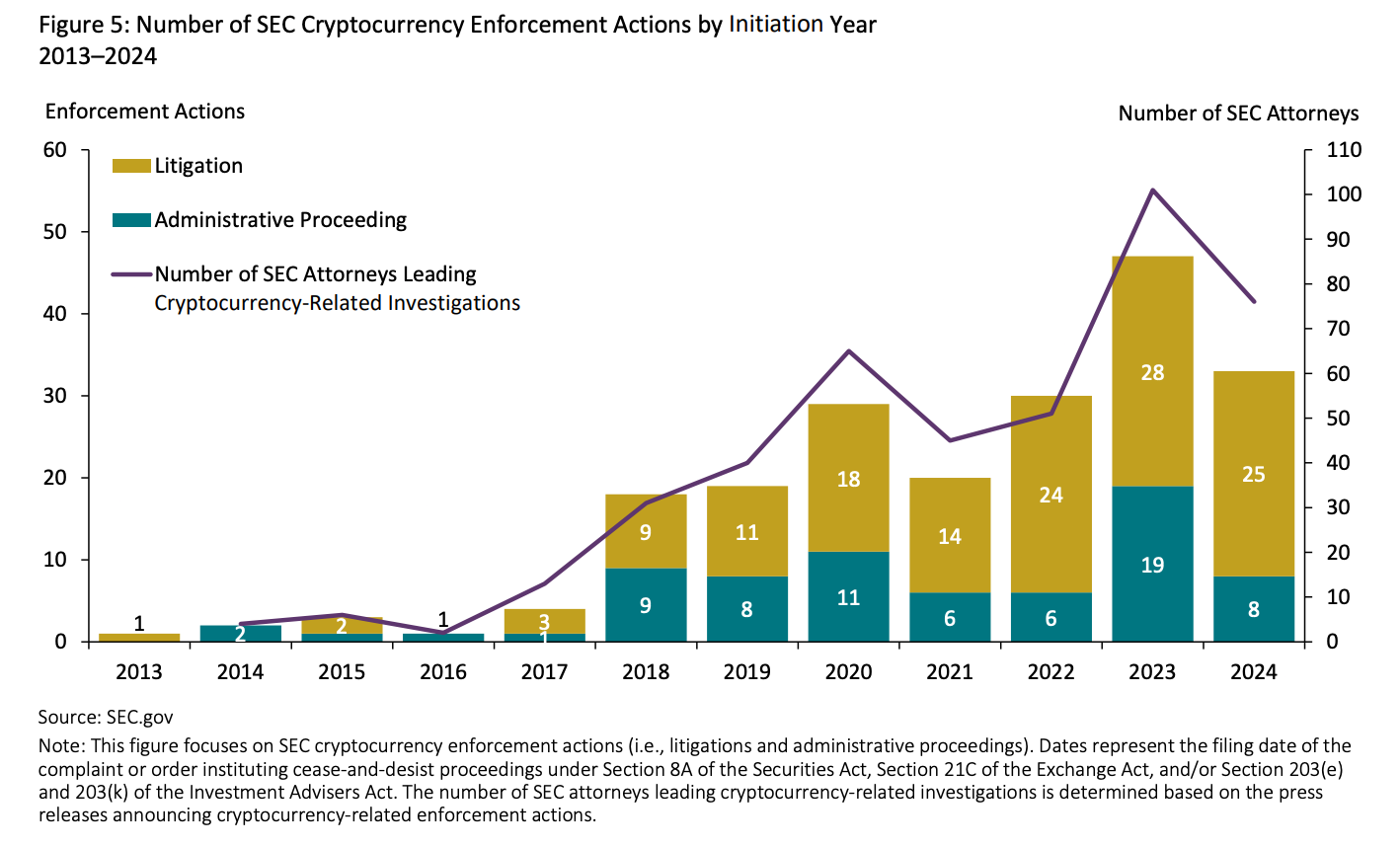

Traders began to speak of the “SEC effect”: a sell-off triggered not by fundamentals, but by enforcement headlines. Talent and capital fled to Europe and Asia, where frameworks like MiCA (EU) or Singapore’s licensing regime at least spelled out what was allowed. In Washington, meanwhile, the SEC kept staffing up—on average 8.3 attorneys per crypto case under Gensler, compared with 5.9 under his predecessor Jay Clayton—reflecting the intensity of this litigation-driven approach.

By early 2025, the strategy had run its course. The new administration dropped the outstanding suits against Coinbase and others, closing the book on the enforcement era. It left behind a trail of uncertainty, stalled innovation, and capital flight. But it also set the stage for a sharp pivot: instead of fighting the industry in court, regulators would attempt to build an architecture for it.

The Spring 2025 Agenda: Building a New Architecture

2025 opened with a clean break. The White House made “crypto capital of the world” a campaign promise and turned it into policy. Regulators were told to stop treating crypto as a problem to punish and start treating it as an industry to structure. A working group laid down the goal: use existing authority to give clarity, attract talent, and keep the United States at the center of blockchain innovation.

The SEC and CFTC responded with twin initiatives—“Project Crypto” and the “Crypto Sprint.” Together they amount to the first attempt at a durable regulatory architecture for digital assets.

Redrawing the map.

The biggest shift came in philosophy. SEC Chair Paul Atkins declared in a landmark speech that “most crypto assets are not securities.”

That single line flipped the old presumption on its head. Instead of assuming nearly every token was a security under Howey, regulators would take a more nuanced view. “Project Crypto” was launched to modernize securities law through rulemaking and guidance, creating space for assets that don’t fit neatly into 20th-century categories.

Safe harbors.

For years, projects launching new networks were trapped—any token distribution risked being treated as a securities sale. The new agenda introduces exemptions and safe harbors. These carve-outs would let networks bootstrap under supervision, with disclosure, and mature toward “sufficient decentralization.” It acknowledges the reality that crypto projects evolve, and that their tokens don’t need to be treated as securities forever.

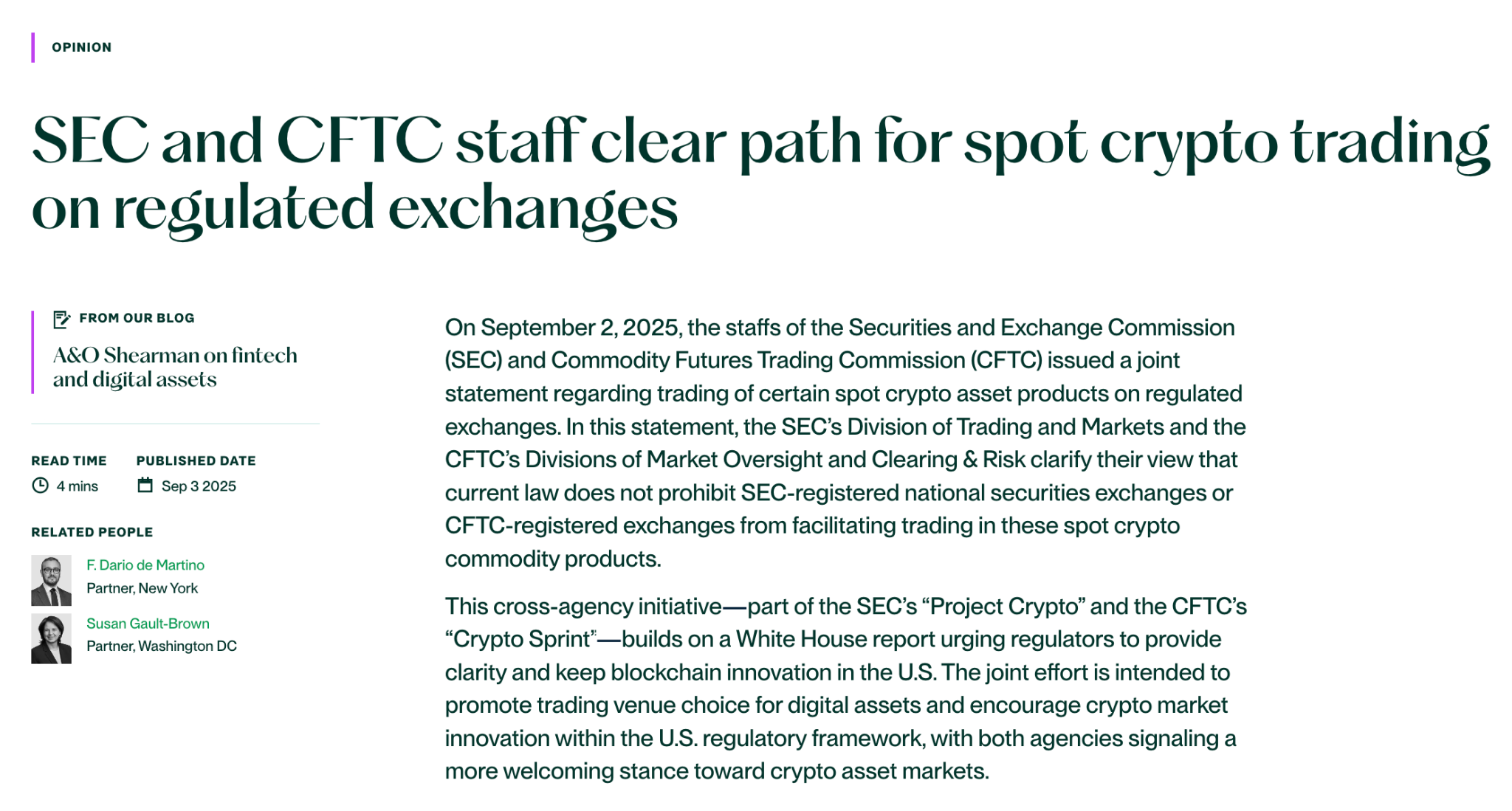

Spot access.

On September 2, 2025, the SEC and CFTC issued a joint statement that electrified markets. They clarified that existing law does not block national exchanges like Nasdaq, NYSE, or CME from listing spot Bitcoin and Ether products.

With guardrails—surveillance, secure custody, transparent trade reporting—the green light was on. For the first time, digital assets were formally welcomed onto the same venues as America’s most established securities and commodities.

Custody unlocked.

Institutional adoption had long been blocked by Staff Accounting Bulletin 121, which forced banks to treat customer crypto as their own liabilities—a capital-intensive poison pill. One of the new regime’s first acts was to rescind SAB 121.4 Then came a directive to adapt custody rules so banks and custodians could safely hold digital assets. This move opened the door for traditional financial institutions to finally enter, giving allocators the institutional-grade security they had been waiting for.

The rise of “super-apps.”

Atkins also pushed staff to design a framework for all-in-one intermediaries. The vision: a single licensed entity offering trading, lending, staking, and custody across securities and non-securities alike. Instead of today’s fragmented mess of overlapping licenses, U.S. firms could provide integrated digital finance experiences under one roof—the kind already popular in Asia.

A cohesive strategy.

Taken together, these steps are a coordinated attempt to integrate crypto into the U.S. financial system. The previous enforcement era had driven talent and trillions in market cap abroad. The new agenda pairs nationalist rhetoric—“American leadership,” “Golden Age of Crypto”—with mechanisms that explicitly favor large, regulated players. Enabling spot ETPs, bank custody, and licensed super-apps points in one direction: pull crypto onto Wall Street’s rails.

This promises stability and investor protection. But it also narrows the field. For most people, the future of crypto in the U.S. will run through familiar financial institutions, not peer-to-peer protocols. The ethos of decentralization isn’t dead, but it now lives at the margins of a system being rapidly absorbed into traditional finance.

A New World Order: The Global Benchmarks

America’s pivot doesn’t exist in isolation. Around the world, other power centers have been racing to shape crypto on their own terms. Three models are emerging: Europe’s “Rulebook,” the U.S./UK’s “Integration,” and Asia’s “Sandbox.”

Europe: the Rulebook.

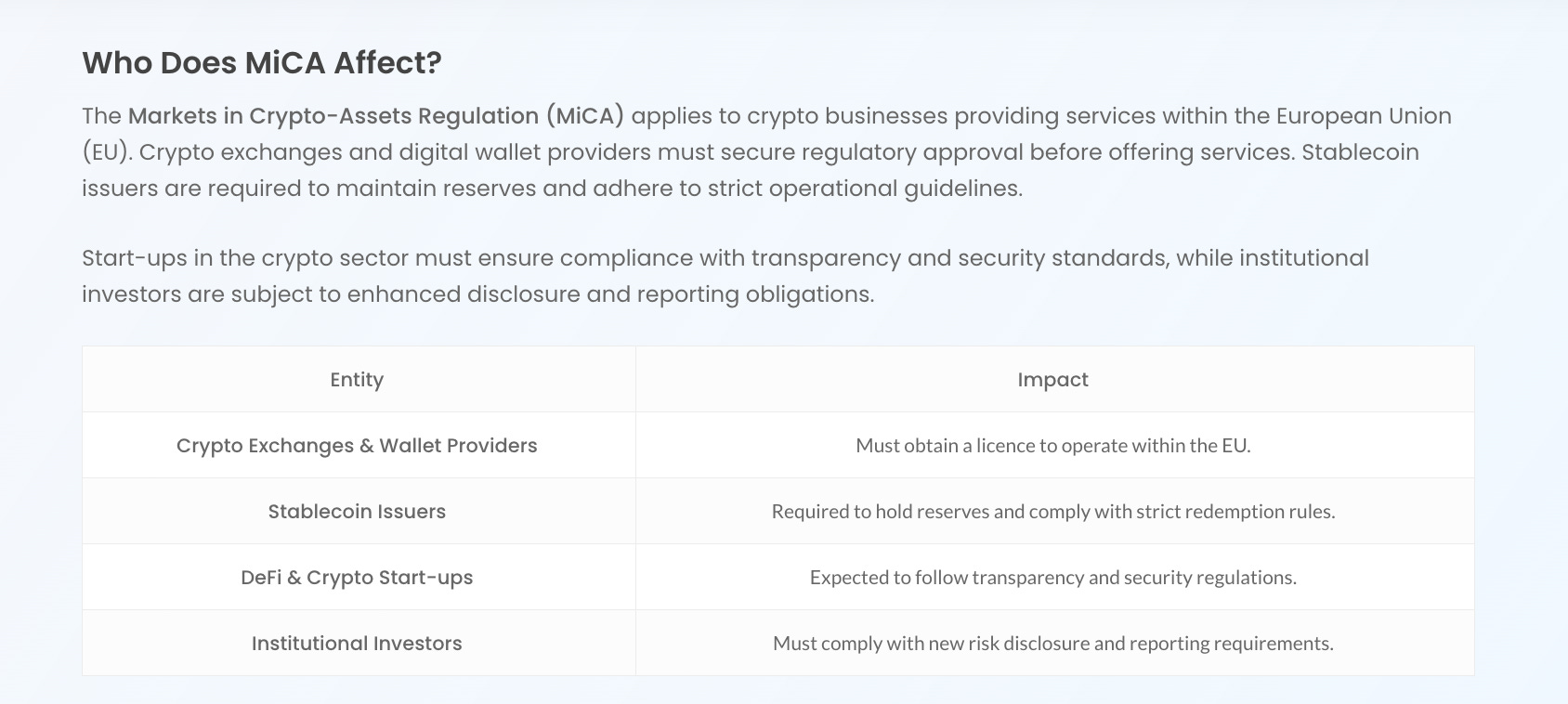

The EU’s Markets in Crypto-Assets (MiCA) framework went live at the end of 2024.28 It is a single, prescriptive code for 27 countries, with strict categories for tokens—asset-referenced, e-money, or otherwise—and a licensing regime that lets firms operate across the bloc once approved. It gives legal certainty but leaves little flexibility. NFTs and DeFi remain outside scope for now.

UK: integration, but deeper.

The UK extended its powerful Financial Services and Markets Act (FSMA) to pull crypto into the existing system. It carved out new activities, including custody and even staking as regulated services. This “MiCA-plus” approach is granular and broad in reach, forcing overseas firms that touch UK retail customers to play by UK rules.

Asia: the sandbox hubs.

Singapore and Hong Kong took a pragmatic path while the U.S. was stuck in lawsuits. Singapore built a tiered licensing system under its Payment Services Act, with tough AML/CFT rules and detailed standards for stablecoins.

Hong Kong re-opened its doors to crypto with a licensing regime for exchanges, recently expanding retail access to major tokens.41,42 Their aim is simple: attract business quickly, update rules iteratively, and establish themselves as global crypto hubs.

China: the anomaly.

China still bans all private crypto trading, mining, and exchange activity.43 Its energy is poured into the digital yuan. Yet the U.S. move on stablecoins, especially the GENIUS Act, is forcing a rethink.

USDT is already widely used inside China to skirt controls, and policymakers are now weighing whether to allow yuan-backed stablecoins—most likely through Hong Kong as a testbed.

Together, these approaches reveal a split world. Europe seeks control through a single code. Asia courts agility and competitiveness. The U.S. is pulling crypto onto Wall Street’s rails, betting that the depth of its capital markets will make its model the global default.

The Market Reacted

Markets are forward-looking. Long before today’s SEC/CFTC joint statement, investors were already behaving as if the pivot had arrived. Each regulatory signal in 2025 — from the January repeal of SAB 121, to the dismissal of the Coinbase lawsuit in March, to the Senate’s passage of the GENIUS Act in June — added fuel. By the time Chair Atkins gave his “Project Crypto” speech in September, capital had clearly decided that the era of “regulation by enforcement” was over.

Institutional flows.

The clearest evidence came in exchange-traded products (ETPs). Year-to-date, more than $35 billion has poured into U.S. crypto ETPs, with Ethereum funds attracting the lion’s share. In August alone, $4.9 billion flowed in — nearly $4 billion of it into ETH products.

That rotation away from Bitcoin and toward Ethereum is a classic sign of rising confidence: once institutions trust the rails, they move further out on the risk curve.

Venture capital returns.

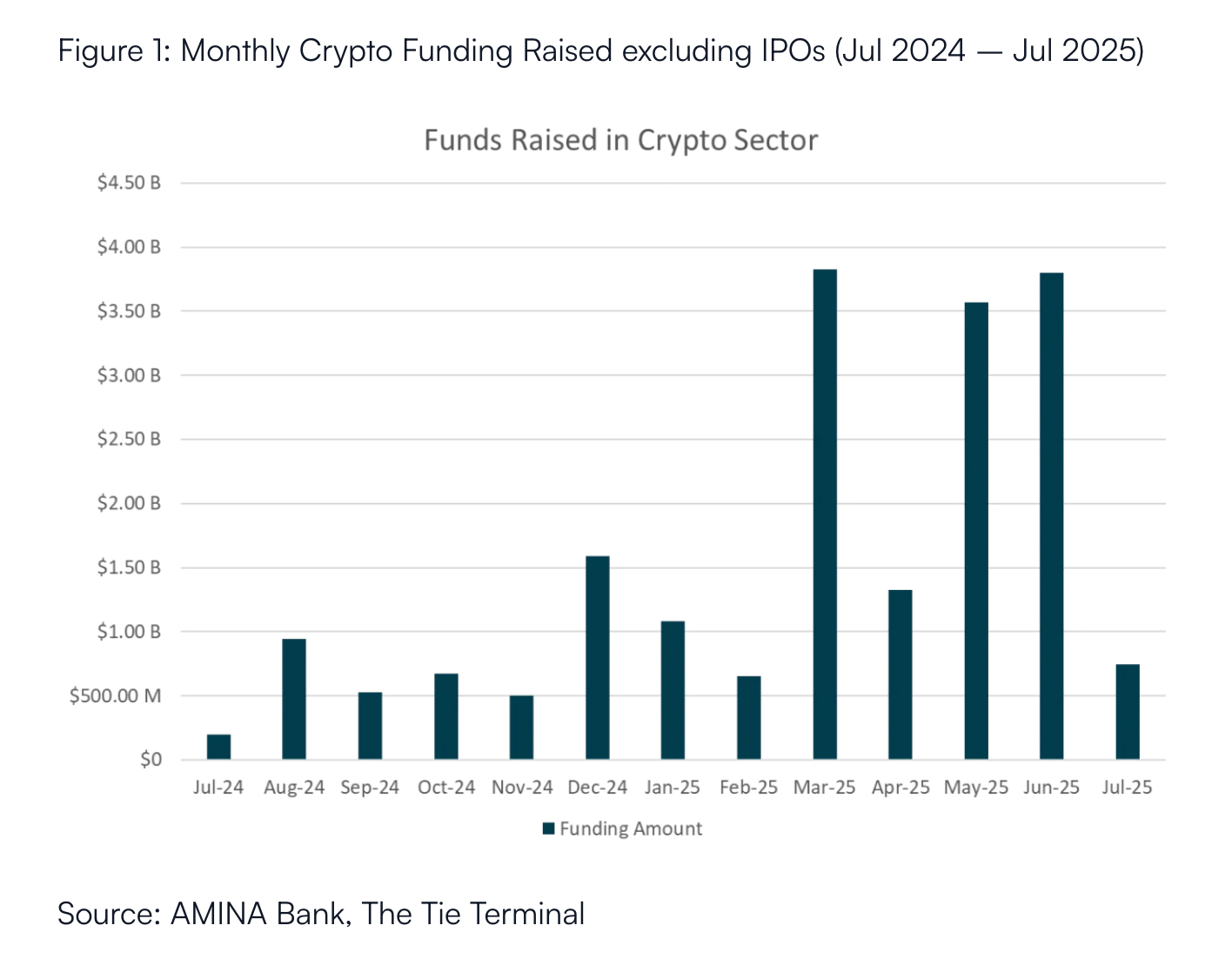

VCs also rediscovered conviction. In Q2 2025, crypto startups raised over $10 billion—double the level of the previous year and the strongest quarter since the 2021 bull run.

Unlike the scattershot bets of that cycle, funding is now more disciplined. Nearly half went into trading venues and compliant infrastructure, signaling that venture money is following the regulatory clarity, not chasing memes.

Grassroots sentiment.

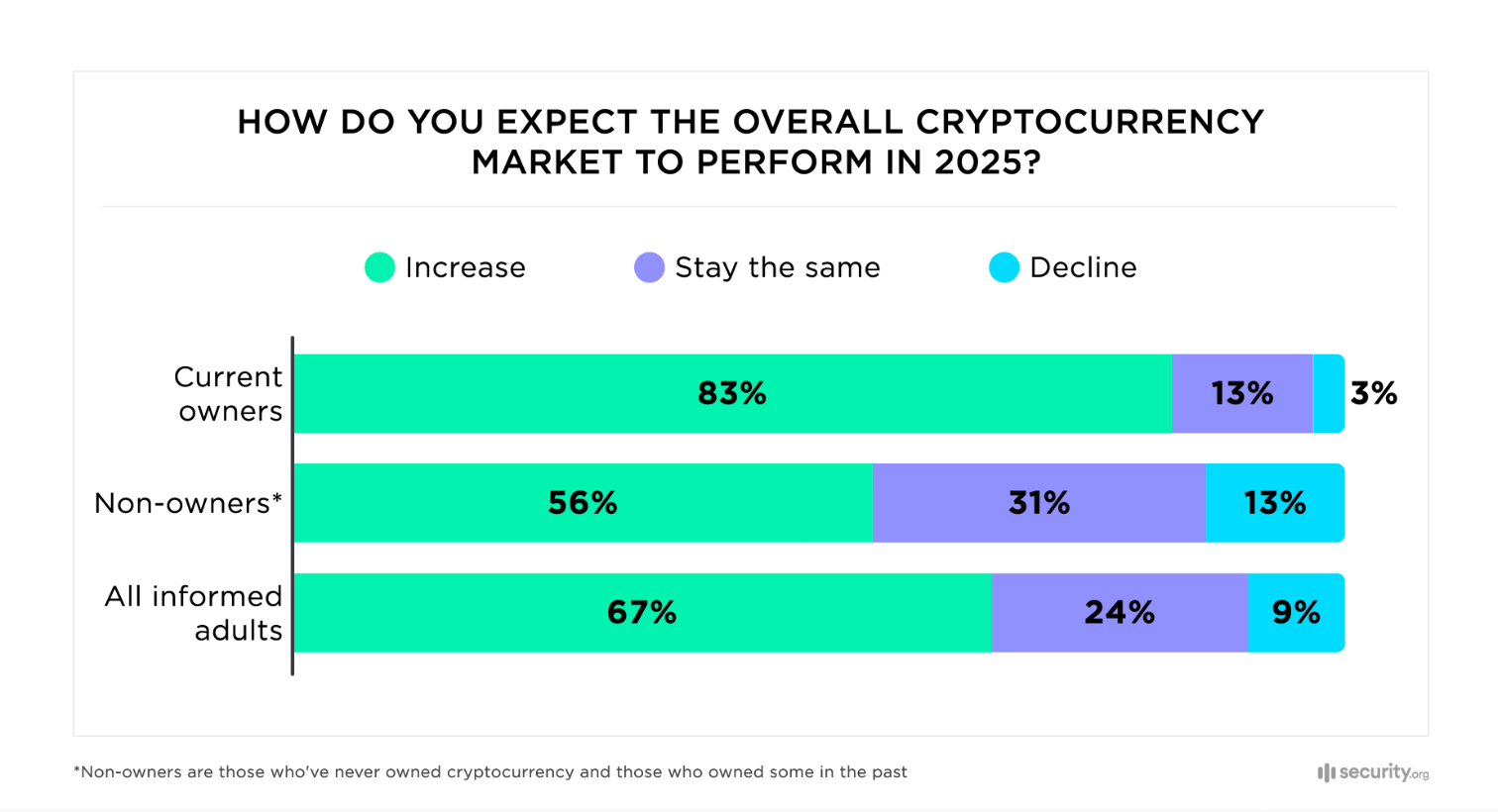

Retail followed suit. Surveys from early summer show U.S. investors more bullish than at any time since 2021: over 60% of Americans familiar with crypto expect it to rise in value during the new presidential term, and two-thirds of current holders plan to buy more.

Put simply: the market read the writing on the wall, and didn’t wait for September’s capstone. Each policy move—rescinding hostile accounting rules, dropping lawsuits, passing stablecoin legislation—pulled more capital off the sidelines. Today’s joint SEC/CFTC announcement only formalizes what investors had already priced in: America is back in the game, and capital is flowing accordingly.

Winners, Losers, and the New Fragilities

Every major rewrite of the rules creates winners, losers, and hidden risks. The U.S. pivot is no exception. It doesn’t just open doors for innovation; it redraws the playing field in ways that favor some players and squeeze others out.

The Winners

The firms best prepared to play by the rules are the ones walking away with the spoils. Coinbase and Kraken, after years of building compliance infrastructure, suddenly look like the natural on-ramps for U.S. capital. The dismissal of the SEC’s case against Coinbase in early 2025 effectively crowned it the default exchange for the domestic market.

Wall Street is another clear beneficiary. The scrapping of SAB 121 and the green light for spot products opened the floodgates for banks and asset managers. Custody, ETFs, in-kind creations—all the bread and butter of traditional finance—are now firmly in play. Giants like BlackRock and Fidelity can bolt crypto onto their existing distribution machines and scoop up market share with ease.

Stablecoin issuers who can meet the strict rules of the new GENIUS Act are also poised for liftoff. Circle’s USDC fits neatly into this mold, with federal oversight turning what was once a regulatory liability into a competitive advantage. The market response was immediate: Coinbase stock jumped on expectations for USDC growth, while Visa and Mastercard shares slipped on fears that stablecoins could undercut card settlement rails.

Tokenized real-world assets ride the same wave. With clearer guidance on what counts as a security and safe harbors for compliant issuance, platforms bringing real estate, private equity, or bonds on-chain now have a defined path forward.

The Losers

Where there are winners, there are casualties. Offshore exchanges built on regulatory arbitrage are on borrowed time. The combination of new rules and stepped-up enforcement—underscored by OKX’s guilty plea and fines in February 2025—means U.S. users are no longer worth the risk.

Algorithmic stablecoins—the dream of “money without collateral”—are effectively outlawed. Without 1:1 backing in liquid reserves, they won’t pass muster in the U.S. market.

Privacy coins face a similar squeeze. Monero, Zcash, and other anonymity-focused assets run directly against the grain of AML and KYC rules. They are likely to continue to be delisted from regulated venues, pushed to the fringes where they trade like the junk bonds of crypto—high risk, tolerated only at the margins.

DeFi at the Crossroads

Decentralized finance faces a fork in the road. On one side is “RegDeFi”: protocols that integrate KYC/AML into smart contracts or front ends, making themselves palatable to institutions. On the other side is the “Wild West”: protocols that cling to permissionlessness but are effectively cut off from mainstream liquidity.

Regulators won’t buy the argument that true decentralization makes something untouchable. As the BIS has argued, there is a “decentralization illusion”: nearly all DeFi projects have pressure points—governance token holders, core devs, or web interfaces—that can be targeted.

That pressure opens the door to regulatory capture. Large, well-funded players—Coinbase, Wall Street banks, and asset managers—are in the best position to shape rulemaking. The risk is that regulations become barriers to entry, locking out smaller innovators. The debate around Coinbase’s lobbying on stablecoin legislation, which could tilt the field against Tether, shows how quickly this dynamic can play out.

A New Kind of Risk

The deeper story is systemic risk. For all its chaos, the old regime had a firewall: when FTX imploded, contagion was largely contained within crypto. The new framework dismantles that firewall. Banks are moving into custody. Stablecoins are entering payment rails. ETFs are tying crypto directly into retirement portfolios.

That means a failure in crypto won’t just hurt crypto anymore. A compromised custody unit at a major bank, a glitch in a systemic ETF, or a sudden collapse of a regulated stablecoin could all ripple back into traditional markets. Ironically, the very rules designed to make crypto safer also make it more tightly coupled to the financial system.

The house has been rebuilt, but the foundations are now tied together. If one shakes, the other will feel it.

Looking Ahead: Paths for 2026 and Beyond

The regulatory turn of 2025 has set the stage, but the play is still unfolding. Three paths seem most plausible as the dust settles.

The Great Integration.

The most likely outcome is that the U.S. succeeds in pulling crypto firmly into its financial system. By 2026, safe harbors for token launches are in place, and the SEC and CFTC have finalized rules for registering digital asset intermediaries. Compliant, dollar-backed stablecoins issued under the GENIUS Act function as a mainstream payment rail, integrated into fintech apps and traditional banking alike. Spot Bitcoin and Ethereum ETPs are routine in portfolios, while banks and asset managers provide custody and investment products at scale. The market consolidates around a few large, regulated exchanges, and DeFi protocols adapt by embedding KYC/AML checks, birthing a “RegDeFi” sector for institutions. Backed by the depth of U.S. capital markets, this framework becomes the de facto global standard, with other jurisdictions aligning to preserve access.

A Fragmented World.

But the U.S. could stumble. Political gridlock, lawsuits, or turf battles between the SEC and CFTC might leave the framework patchy and hard to follow. In that case, Europe’s harmonized MiCA rulebook could cement the EU as the hub for large-scale, compliant crypto, while Singapore and Hong Kong continue to lure high-growth projects through their agile sandbox regimes. The result would be a fractured market with three distinct regulatory orbits and little interoperability, forcing firms to silo operations region by region.

A Decentralized Resurgence.

There is also the contrarian outcome: over-centralization sparks a backlash. If regulation bends too far toward incumbents, recreating the inefficiencies of Wall Street with higher fees and fewer choices, developers and users could exit en masse. Advances in zero-knowledge proofs, decentralized identity, and cross-chain tech could fuel a vibrant, censorship-resistant parallel economy. This world would not replace the regulated system but grow alongside it, offering sovereignty and resilience outside the reach of any single state.

Conclusion: The Great Integration Begins

The meaning of the pivot depends on where you stand. To the public, it is about safety and stability. To investors, it is legitimacy and access. To builders, it is a long-awaited roadmap. And to policymakers, it is a geopolitical play to reassert U.S. dominance in financial technology.

Together, these perspectives capture the essence of what has just begun: the Great Integration of crypto into the heart of the U.S. financial system—and the risks, tensions, and countercurrents that will shape its next chapter.